Romance is in the air for Valentine’s Day, and we encourage you to check out our recently released personal finance module titled Romance and Money. Here’s a free preview with a downloadable Money Date Guide at the bottom!

Planning money with a partner involves trust, patience, dedication, understanding, and the ability to communicate. We commonly discuss how to improve your personal relationship and psychology with money. Now it’s time to become a team player. Remember these common phrases:

Two heads are better than one.

Teamwork makes the dream work.

Having the chance to build your financial life alongside a partner can help in many ways. Here are a few examples:

Shared responsibilities and expenses

Specializing in particular financial roles for the family

Diversified income streams

The chance to organize, collaborate, and focus on shared financial goals

Yet, involving another person’s money dynamics, behaviors, habits, and philosophies can cause challenges.

Money’s Cloud Over Couples

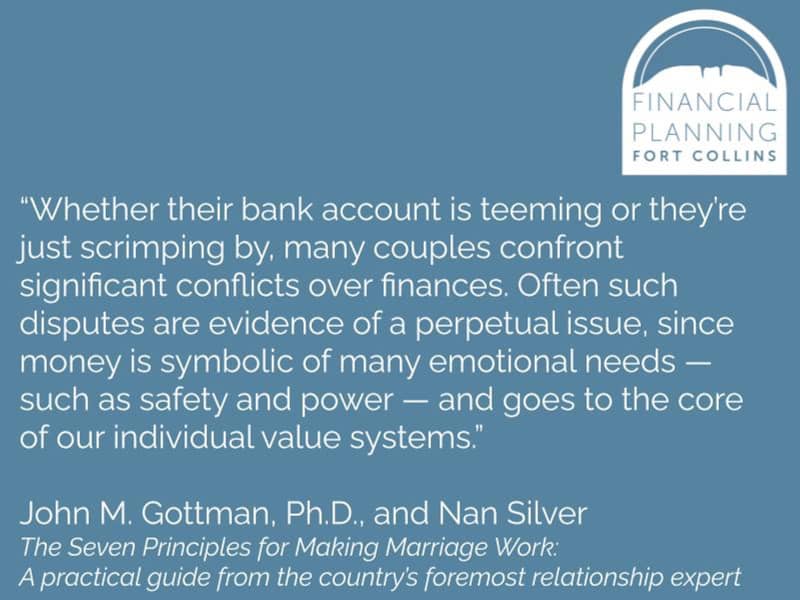

Money can cause tension, and it doesn’t help that society sees financial topics as taboo, which can make talking about money feel uncomfortable. As John M. Gottman, Ph.D., and Nan Silver wrote in their book, “The Seven Principles for Making Marriage Work”:

A study titled “Reasons for Divorce and Recollections of Premarital Intervention: Implications for Improving Relationship Education” lists “financial problems” as the third most common issue that led those in the study to divorce. The two higher-ranking categories were “growing apart” and “infidelity.”

According to the study, “financial difficulties were not the most pertinent reason for their divorce, but instead contributed to increased stress and tension within the relationship.”

Growing apart happens to some couples over time, and infidelity is an action. Yet money decisions are part of day-to-day life. This tension and stress can compound over time if partners don’t address it and communicate.

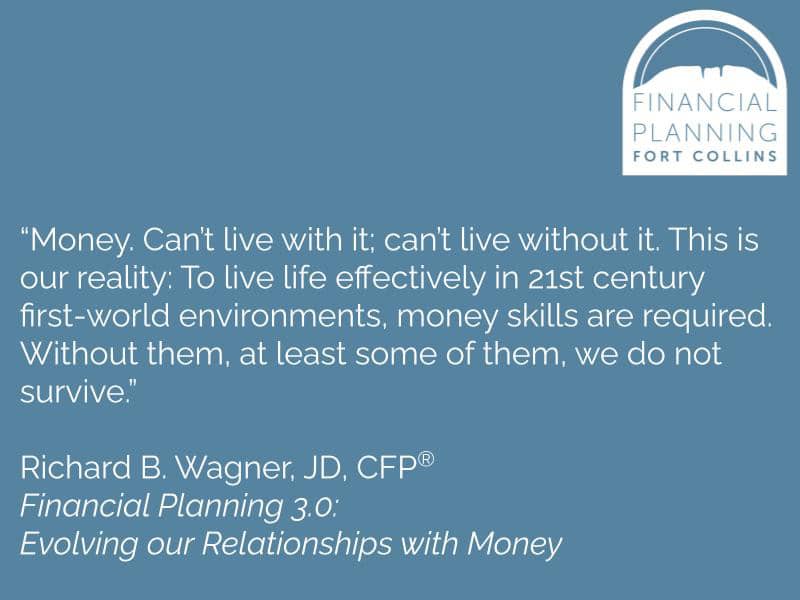

As Dick Wagner says in his book, “Financial Planning 3.0: Evolving our Relationships with Money”:

Instead of letting money cloud your relationship, we encourage you and your partner to get financially naked with one another. Get on the same page about money by opening up about your money philosophies and goals. You two can then become a united team as you tackle your financial planning tasks together.

Some tension and stress will inevitably surface around money because money can be stressful. Yet you can have someone in your corner to work alongside you as you improve your financial situation over time.

Open Up With Your Partner

Open Communication About Finances

It’s best to be open, transparent, and forthcoming about finances with your partner. This can help you establish trust, which can build over time — just like the compound interest in your financial lives.

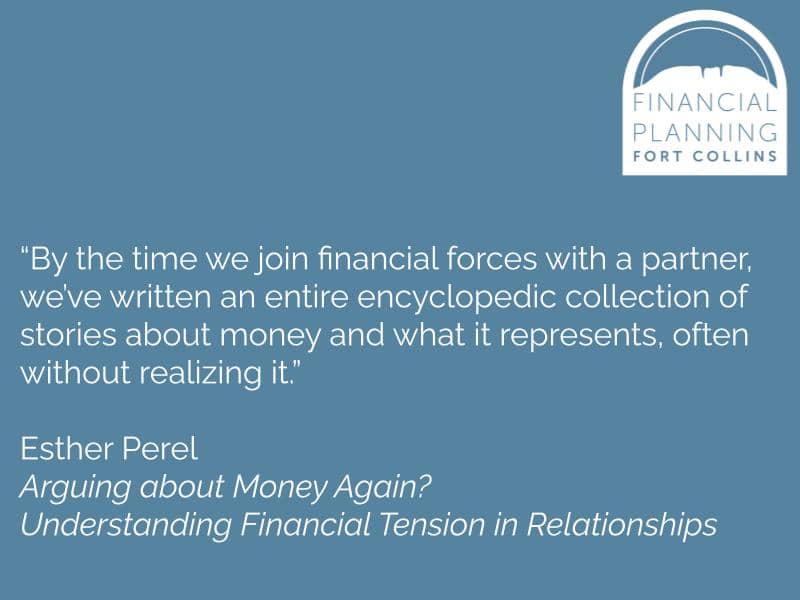

Money’s taboo nature can make discussing this topic uncomfortable, emotional, and difficult. And we all have money histories, as the following quote illustrates:

Esther Perel delivered TED Talks about her experiences as a couples therapist. She also shares her insights on how to address money with your partner in her article, “Arguing about Money Again? Understanding Financial Tension in Relationships.”

Perel encourages her clients to think of financial discussions as time to reprioritize their lives. As financial planners, we choose to build on her wisdom by asking you to reprioritize your financial plan alongside your chosen partner.

Your money decisions illustrate your values. You spend and save money in ways that may be seen as your priorities.

You choose to save your money for your retirement because this life responsibility is important to you.

You choose to spend money on lavish gifts for your partner because this is how you demonstrate your affection.

You choose to invest money for your children’s education because you want to support their future places in the world.

You have ingrained values around money that you’ve nurtured over time. Your partner does, too. As you two become a united team in addressing your money life together, we encourage you to communicate about money on a deeper level.

Opening Up About Money with Your Partner

We provide a guide later in this module with some objective and subjective questions regarding money. This can help you and your partner better understand each other’s money histories, habits, and goals while also determining how to move forward with your individual and joint money lives.

But we’ll get into more detail in this section to illustrate the reasons why you should be open with your partner about your financial data, circumstances, beliefs, and values.

▶︎ Prevent Lopsided Dynamics

Money has power in our society. Money can also create unequal power in a relationship. Money conversations and planning can alleviate one person from gaining too much power in a relationship and avoid making the other person feel like a subordinate.

We discussed some studied money disorders in our Money Psychology module (Money Psychology > Family Money Troubles). The common money disorders that fall into this category are:

Financial Infidelity: There’s trouble trusting a partner when it comes to managing shared money

Financial Abuse: Money is used to control another person’s behavior

Financial Enabling: Saving loved ones whenever they get into money trouble

Financial Dependency: Struggling to support oneself and consistently relying on others

These are serious issues that you can hopefully avoid by being in open communication with your partner. Yet, when these troubles surface, it’s best to seek outside professionals to guide you in therapy and/or legal guidance.

▶︎ Establish Financial Continuity Plans

In some couples, one party controls all money decisions while the other focuses on other areas. This is especially common in older generations as this was the societal norm of times past. We’ve seen many times in our financial planning experience, as these couples get older, that men are more likely to die first in husband-and-wife relationships. This leaves the widow with wide-eyed confusion as she goes through the learning curve to:

Pay the bills.

Access financial accounts.

Implement the estate plan.

Complete a wide variety of other tasks that add stress and a sense of being overwhelmed.

Many times, other parties (like adult children) step up to help facilitate the transition — or insert themselves into a similar role as the recently deceased party. But we also see that many couples are preparing for these situations earlier in their relationships.

By discussing your finances with your partner, you can establish plans and expectations with what to do in times of income disruption, disability, and death. By having both parties engaged in the financial management of the household, a foundation of money management exists for a partner to step up in times of need. This confidence and skill set can be instrumental as the spouse confronts the new learning curves of addressing the financial tasks that the now-unavailable partner previously handled.

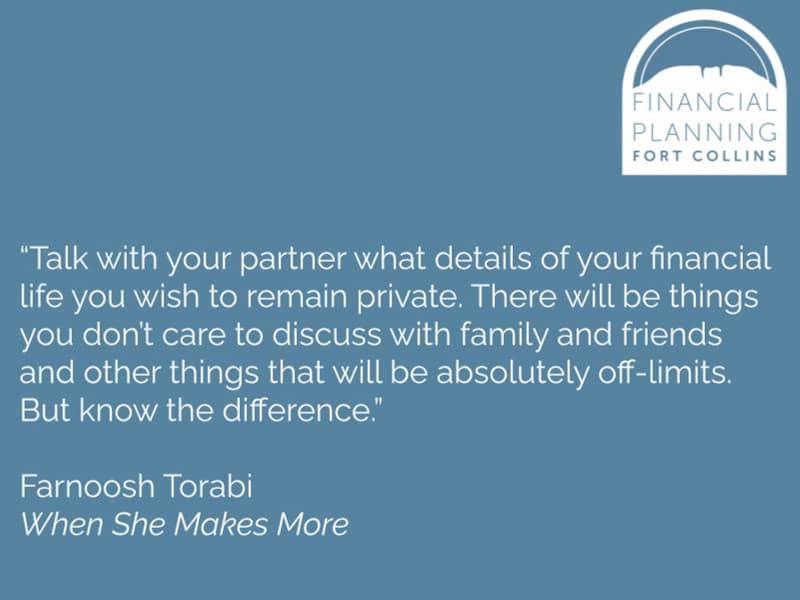

▶︎ Understand Boundaries

Money habits can have feelings of shame attached to them. For example, if I ever need a fast food moment, I typically make my purchase in cash — so the transaction isn’t logged in my and my wife’s joint credit card history!

Open dialogue about money can help you and your partner decide what you need to share with the other partner, what’s not necessary to share, and what’s off-limits to share with family and friends.

▶︎ Establish Thresholds

Getting on the same page with your partner can give you some freedom. You and your partner can establish thresholds and limits in multiple financial areas that will trigger financial discussions. For example:

Agree to the dollar amount of a purchase that will automatically trigger a financial discussion (for example, you need to review any purchase over $200 together).

Establish a minimum amount to have in your savings account as an emergency fund and understand when to access this money.

What debt limit is your household willing to accept?

What’s your gift-giving philosophy and budget for each other, children, family, friends, and charity?

These examples can give you a sense of freedom to work within your unique family’s culture. You can give yourself permission to follow your intended plan relevant for your partnership, thus hopefully avoiding anxiety and irritating your partner when following these communicated financial limits.

▶︎ Gain a Financial Partner in Pursuing Goals

Many experience their financial lives without much planning, strategy, or limits. Many people “wing it” and get to where they’re going without taking any aim. So they drift and react to critical money moments when they arise.

Beginning an open dialogue with your partner to plan your money lives can help you gain purpose in your financial plan. Your life plan becomes clearer, and you start positioning your finances to reflect your ideal values and financial goals.

Being open with your partner can help you both feel more confident on which life path you take so you can avoid the popular exchange between Alice and the Cheshire Cat in Lewis Carroll’s “Alice’s Adventures in Wonderland”:

This article is a free preview of our FPFoCo Academy. As our client, you can access the rest of this module, which includes:

▶︎ Money’s Role In Relationships (in this article)

▶︎ Open Up With Your Partner (in this article)

▶︎ Divvy Up Financial Roles

▶︎ Strip Down To Your Data

▶︎ Money Management Styles for Couples

▶︎ Tools and Third-Party Assistance

▶ Money Date Guide: Let’s Get Fiscal (see below!)

We encourage you to have a money date with your partner. Talking about money can get uncomfortable, so we created a guide you can use as you discuss the personal side of money, your data, and your shared financial goals.