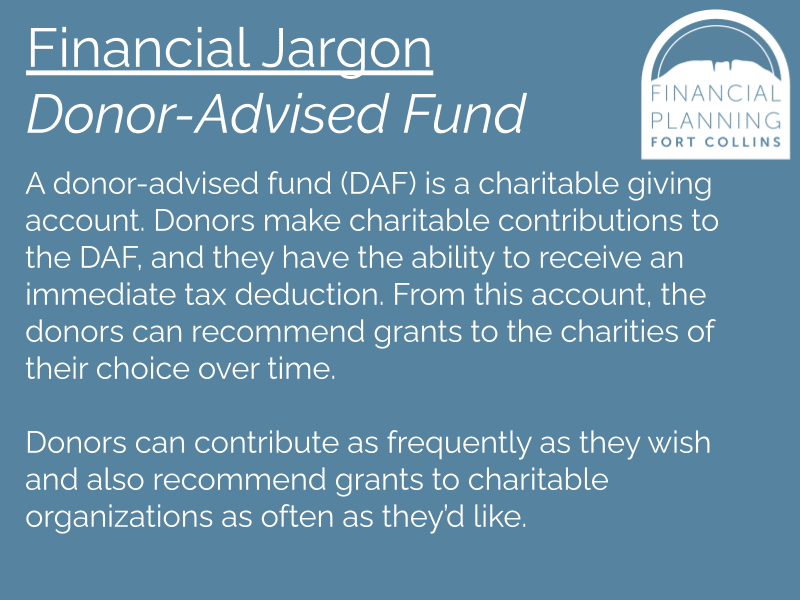

Donor-Advised Funds: 6 Reasons Why I Like Having One

As a financial planner, I try to practice what I preach. Touting the benefits of charitable giving and the tools available to facilitate donations is part of my mission when guiding clients. One charitable giving tool that is becoming more and more popular is a donor-advised fund (DAF). I have one, and I’d like to tell you why you should consider having one, too.

After my family’s experience with a DAF, I can confidently say that using this charitable giving tool has optimized our giving strategy. Let me share with you the six benefits that my family and I personally enjoy.

1. Centralized Giving Location

Tracking down charitable giving receipts can be a pain! Using our family DAF allows us the opportunity to give from a single place from which we can easily track our charitable giving come tax time. Gone are the days of searching for receipts through our email inboxes or bank accounts.

2. Ability to Make Anonymous Gifts

During the early days of the COVID pandemic, a family member graciously asked for no holiday gifts. Instead, they asked for donations to their local community foundation that had programs to help those most affected by the pandemic. My wife and I decided to give directly (meaning not from our DAF) to that local community foundation. It was local for my family member — but not local for us. We now receive way too much physical mail as well as too many emails and phone calls because we’re on this community foundation’s list of donors.

Giving through a DAF allows us to mark our grants “anonymous.” Charities then receive our money without any of our DAF’s details. We don’t end up on donor lists, so we don’t receive any follow-ups.

We can now confidently give to organizations without becoming an administrative burden like we were when placing small donations. This comes in handy when friends are asking for donations to the marathons or other events that make us want to give to specific causes.

I know this is Peanut Butter Philanthropy, but I can’t help myself sometimes.

3. Options to Invest

Compound interest and time in the market will hopefully grow my family’s nest egg over time. The same can be said for my family’s DAF. We’re able to put the money we contribute into investments inside the DAF so those dollars can hopefully grow over time.

If it does, this gives us more money to give. Plus, we won’t need to pay taxes on the profitable investments within the DAF. In addition, we hope that this family DAF will grow and allow our next generation to make more significant donations to the causes important to them.

4. Ability to Receive Complex Assets

I’m not an individual stock picker or advocate for investing in individual stocks. My investment philosophy involves controlling what I can control:

- Keep investment costs low.

- Invest in many things for the sake of diversification.

- Be tax-efficient where and when I can.

- Continue to check in on my asset mix with rebalancing.

- Stay the course when things get nerve-wracking.

I’m not a big fan of individual stocks because it’s difficult to know the ins and outs of all the companies and investment options out there. That’s why I like investing in low-cost ETFs that passively follow indices.

I had a decision to make when my grandfather generously gifted me some individual stock positions. I could sell the positions and then put the proceeds into some low-cost ETFs. However, I would’ve needed to realize the capital gains associated because the positions had increased in value since he’d originally bought them. I then realized that my family’s giving goal for the year was about the same amount as the value of the stock positions. An opportunity presented itself!

I chose to gift the individual stock positions to my family’s DAF. This allowed me to avoid the capital gains and gift the full value of the stock. If I’d sold the stock and then gifted the amount to a charity, I would have lost some of the money to capital gains taxes. This opportunity allowed more of the stock value to go to charity and keep the money that we would have otherwise donated in my family’s checking account. Plus, I stayed true to my investment philosophy and our annual giving plan.

To learn more about how to give complex assets like stocks that have gone up in value — and also give in a tax-efficient way — here’s a webinar from two charitable giving experts:

5. Automatic and Spaced-Out Donations

Instead of being on the to-do list, my family can designate automatic grants to be sent from our DAF to the charitable organizations we choose to support on an ongoing basis. This comes in handy as it helps us follow through on our charitable giving intentions. Plus, we’re satisfied when we receive the confirmation emails that our grants were released. These emails are certainly much better to see than the automatic payment confirmations for our streaming subscriptions!

After learning more about effective altruism, we couldn’t help to support organizations through our family DAF on a recurring basis. Effective altruism promotes that charitable giving shouldn’t be seen through the eyes of personal satisfaction but as a way to give money so it can do the most good. I’m an advocate of doing both, and my family chooses to do both by scheduling recurring grants from our DAF.

If you’re interested in learning more about the effective altruism methodology, here’s a TED talk from one of this movement’s pioneers. This is a controversial topic, and there are some controversial messengers. However, the effective altruism movement aims to give through “the heart and the head” with the premise that all lives are equal and have value.

6. Family Giving Account

One aspect of my family’s DAF is the ability to name successors. These are individuals who we can name to take over future grantmaking abilities from the Andrews Family DAF. My wife and I are the first level of decision-makers. We’re also naming our children as the individuals who will make decisions when we pass. This gives us the confidence that charitable giving will be an ongoing theme throughout our kids’ lives — and we hope that it will seep into our next generation’s values.

Of course, I don’t hope that my kids are the sole-decision makers anytime soon! But it’s nice to know that this DAF will become their responsibility when I’m no longer living. In the meantime, we’re excited to have family meetings to decide which causes receive grants from our family DAF.

To Recap

There are many charitable giving tools out there, and none is “one size fits all.” A DAF is an optimal tool for my family, but I encourage you to find a giving strategy that makes sense for you. And then, more importantly, commit to positively influencing the causes important to you.

If the DAF is a giving method that suits you, here’s a recap of the six benefits I shared throughout this article:

1. Centralized giving location

2. Ability to make anonymous gifts

3. Options to invest

4. Ability to receive complex assets

5. Automated and spaced-out donations

6. Family giving account

As with anything, there are pros and cons. We have another article that goes into the intricacies of DAFs and how they compare to private foundations and community foundations called How to Give Better: Community Foundations, Private Foundations, and Donor-Advised Funds.

Let’s Talk Charitable Giving

If you want to have a conversation around charitable giving and how it can influence your financial plan, please schedule a charitable giving meeting with me.

And, if you’re not yet a client but want to have a conversation around charitable giving, I invite you to get started by scheduling a conversation with me. I’d be thrilled to help you if you’re interested in how you can give better!

Not a client yet? See if our ensemble approach is right for you.